Filing for bankruptcy can offer a fresh financial start once when other options for debt relief aren’t doing the job. It allows you to discharge all or most of your existing debts, so you can move forward free of the financial burden. This guide will tell you everything you need to know about a Chapter 7 bankruptcy filing, so you can decide if it’s the right solution to help you get a fresh start with your finances.

Know This:

- In Chapter 7 bankruptcy, the court sells your assets to pay off the creditors you owe. This doesn’t mean you have to sell everything you own. For example, if your house falls below a certain value, you can keep it.

- Filing for Chapter 7 only takes four to six months to complete. However, it will stay on your credit report for ten years from the date of filing.

- Some debts (such as child support, civil lawsuit debts, or “new” tax debt) cannot be discharged in Chapter 7 bankruptcy.

What is Chapter 7 bankruptcy?

Chapter 7 is one of two types of personal bankruptcy filings. It’s also called “liquidation bankruptcy” because the court liquidates (sells) your assets to pay off your lenders and creditors. This allows you to complete your filing quickly, so you can get a fresh start faster. Once the court liquidates your assets and pays the proceeds to everyone you owe, the court discharges any remaining balances.

It’s important to note that asset liquidation is rarely as scary or as damaging as it sounds. First, the court will not sell off everything you own. Things like clothes and personal property, tools for your business and even 401(k) retirement savings are all exempt. Even your home and your car may qualify for an exemption as long as they fall below a certain value.

In truth, most people who file for Chapter 7 never face any asset liquidation at all. They enjoy the fast, clean exit and still get to keep their stuff.

How does Chapter 7 work?

- First, you must complete mandatory pre-bankruptcy credit counseling within 180 days of when you want to file.

- Once you receive your certificate, you can proceed to file. You must provide:

- Your pre-bankruptcy credit counseling completion certificate

- A schedule of assets and liabilities – i.e. what you own and what you owe

- A schedule of income and expenditures – i.e. what you make versus what you spend

- A statement of financial affairs – a report of any lawsuits, repossessions, foreclosures and property liens

- A schedule of executory contracts and unexpired leases – basically, any contract agreement you have that hasn’t been completed

- After the court receives all the documentation required, they assign a trustee whom you will meet within 15-20 days.

- You will be subject to a means test to verify that you are eligible for Chapter 7.

- At the same time, the trustee issues an “automatic stay” on all your financial accounts. This stay:

- Prevents collection actions on any of your debts

- Stops any current foreclosure actions

- Freezes pending civil lawsuits, such as collection suits

- Your creditors then have the opportunity to object to discharge if they can prove you committed fraud.

- Once the trustee addresses all objections, you receive your official final discharge.

When to file for Chapter 7 bankruptcy

Filing for bankruptcy can be expensive and emotionally draining. How do you know when to pull the trigger and talk to an attorney? Here are a few ways to tell:

You’ve exhausted all other options.

Even though bankruptcy can be good for some people, it should still be a last resort because your credit will take a major hit. Look into these options first.

Debt consolidation loans

You can use a personal loan to pay off all your debts, consolidating your bills into one monthly payment. Depending on your credit score, a debt consolidation loan could save you money in interest charges. The loan’s interest rate could be significantly lower than the rates of your credit cards.

Before signing on the loan, make sure you can afford the monthly payments. Otherwise, you will fall behind on this, too.

Debt management program

When you call a credit counselor, they help you find the best debt solution for you. This could be a debt management program (DMP) that you enroll in through the counseling agency.

A DMP can lower your interest rates and consolidate your payments, making it easier for you to pay off your debt quicker. This is the best option if you want to maintain a good credit score.

Debt settlement

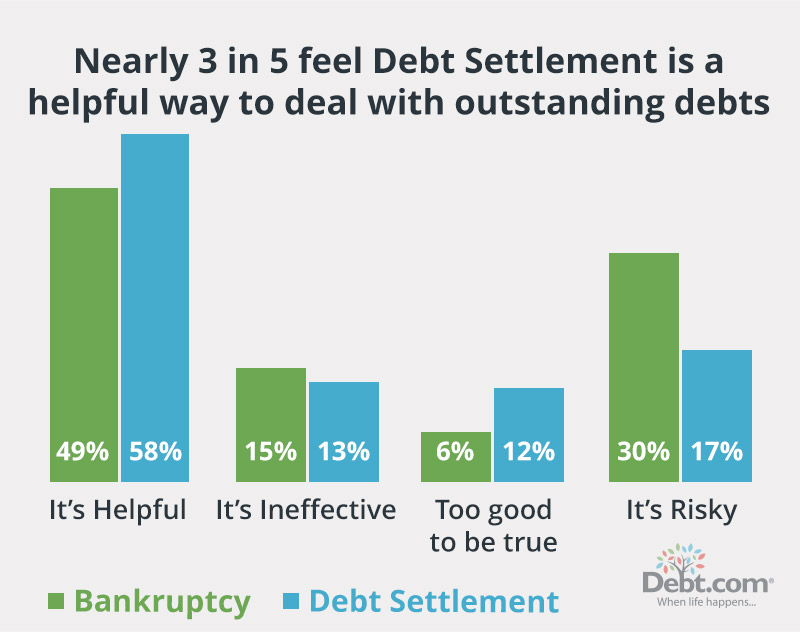

Settling your debt means paying less than what you owe – which means your credit will take a hit. You can either settle your debts on your own by speaking with your different creditors or work with a settlement agency that will consolidate your payments. Debt.com’s in-house research team has surveyed 1,000 Americans on how they feel about filing for bankruptcy or using a debt settlement program.

More respondents said debt settlement is “a helpful way to deal with outstanding debts” and that filing for bankruptcy is risky.

Everyone’s debt situation is different. It’s important to consult professionals before making a decision. A reputable company will always give a free initial consultation before making you commit to a program.

You want to get rid of your debt as fast as possible

Chapter 7 bankruptcy is one of the fastest ways to get out of debt. It will be faster than debt consolidation, a DMP, and most types of debt settlement.

If you want your debt gone – and fast – take a look at the Chapter 7 timeline below.

How long does Chapter 7 take?

The standard timeline for a Chapter 7 filing takes between four to six months to complete.

Keep in mind that you must complete the pre-bankruptcy credit counseling session first. Your certificate must be dated within 180 days of the date you file. So, once you receive certification, you have about 6 months to file.

Following that, first important time marker is the time it takes your trustee to contact you. From the time you file, you can expect contact within about 15-20 days once they review your case. Then, following that initial contact, the remaining process takes about 60-120 days for the trustee to do their work. The time varies based on the complexity of your case and how many creditors file discharged objections. If you have a large number of objections, your case could take longer.

Still, the average person can expect to have a Chapter 7 filing completed within six months. This is much shorter than the time a Chapter 13 filing takes.

Realistically, you could never repay everything you owe.

The alternatives above can all help consumers get out of debt. But can you afford them? Sometimes, your debt is so large that it would be difficult – or impossible – to make the monthly payments.

Be honest with yourself. If you can’t afford to pay down your debt even with reduced interest rates, Chapter 7 bankruptcy may be your best option. Even Chapter 13 has a repayment plan you would have to stick to.

Chapter 7 vs. Chapter 13

If you’re not sure which type of filing you should use, here’s a quick comparison:

| Chapter 7 | Chapter 13 | |

|---|---|---|

| Commonly called: | Liquidation bankruptcy | Wage earner bankruptcy |

| How it settles your debts: | Sells available assets that don’t qualify for exemption for lump-sum payoff | Sets up a monthly repayment plan |

| How long it takes: | About 90-120 days | Up to 5 years, depending on your repayment plan |

| Credit report listing | 10 years from the date of filing | 7 years from the date of filing |

How to qualify for bankruptcy Chapter 7

The Bankruptcy Abuse and Consumer Protection Act of 2005 added a “means test” to the personal bankruptcy filing process. This test allows your court-appointed trustee to review your financial history and make sure your filing is legitimate. This ensures you qualify for Chapter 7 and can move forward with your filing. It also allows the trustee to see if you tried to game the system before you filed.

This may sound scary, but if you are legitimately having trouble then you shouldn’t have anything to worry about. The only cause for concern happens if you don’t really need to file and you’re just looking for an “easy way out.” There can also be issues if you ran up a large volume of debt just before you filed. This is usually taken as a sign of fraud. Even so, you may still be able to file if you can prove your case.

The first part of the means test involves a median income assessment. The trustee compares your income earned over the past 6 months to the median income in your state. They basically compare your income to the Federal Poverty Line for your state.

Then they look at your financial history to see what you owe and what obligations you pay each month. The idea is to make sure that you really need bankruptcy, and specifically need Chapter 7. If you can afford a repayment plan, the court may adjust your filing to Chapter 13. High-income earners are typically under more scrutiny.

In addition to passing the means test, the other requirement for filing is pre-bankruptcy credit counseling. This is simply a credit counseling session that lasts 60 to 90 minutes. You can complete the session in person, over the phone or online. There’s usually a fee between $20-$40.

Let Debt.com connect you with an accredited counseling agency.

Debts that may not be discharged during Chapter 7 bankruptcy

No matter which type of filing you choose, there are certain debts that cannot be discharged bankruptcy. Other debts are not always easily discharged, although it is possible. This is where working with a reputable attorney comes in handy, because they know how to get through your filing quickly with the least amount of lingering debt. After all, your goal is to get a fresh start, so the last thing you want is to have debt that you’re still required to repay!

Here is a list of debts that don’t typically qualify for discharge:

- Alimony and spousal support

- Child support

- Debts to government agencies for fines and penalties, such as court costs

- Civil lawsuit debts for injury to another person

- “New” tax debt

Things like alimony and child support almost never qualify for discharge. If you can’t afford the payments even after your final discharge, then you must seek a modification. In other words, you can modify your monthly obligation moving forward, but you can’t change what you already owe.

Tax debt can only be discharged if it is more than three years old.

The government is also not fond of letting you off the hook for any debts that they’ve ordered you to pay. So, court fines and civil penalties they’ve already assigned to you can’t be easily discharged either. In order to discharge these types of debt, you must be able to show that not discharging the debt will keep you in financial hardship even after your other debts are discharged.

Can you discharge student loans in Chapter 7 bankruptcy?

There’s a common myth that you can’t discharge student loans during bankruptcy. And while it’s true that it can be difficult, it’s certainly not impossible. But the truth is most people don’t even try because they believe student loan debt is not eligible for discharge.

The myth is somewhat rooted in fact. Federal student loans are government-backed, so if you discharge the debt during bankruptcy, the government would be on the hook to cover the lender’s losses. They’re usually not keen to do that. In addition, private student lenders lobbied that their debts should also be protected from bankruptcy discharge to prevent people from taking out loans for education that they have no intention of repaying. So, both federal and private student loans are not as easily discharged as other debts, like credit card debt.

However, there are actually two ways you can go about getting a bankruptcy court to discharge student loan debt:

- If you can prove that not discharging the student loan debt will cause you financial hardship after you complete your filing, then the debt may be discharged. This is true for both federal and private student loan debt.

- For private student loans, you can also get granted discharge for any loans used for an educational program that’s not Title IV qualified. Many trade and vocational programs are not Title IV qualified, meaning that the debt is not exempt from discharge.

So. although it’s not guaranteed that you’ll get all your student debt discharged, it’s at least worth it to try. Even if only some of your loans qualify for discharge, that’s less debt you’ll have to worry about after bankruptcy.

What can you keep after declaring Chapter 7 bankruptcy?

Bankruptcy exemptions vary from state to state, although there are also federal exemptions. Exemptions allow you to keep certain property so that you’re not destitute after final discharge.

By federal law, none of the following possessions are ever liquidated during Chapter 7:

- Clothes, household goods and personal possessions – like musical instruments – up to $600 per item and up to $12,625 total

- Jewelry up to $1,600 total

- Work equipment and tools of the trade up to $2,375 in value

- Pets (and crops, if you have crops)

- A motor vehicle up to $3,775 in total value

- Health aids and medical equipment

- IRAs and Roth IRAs up to $1,283,025

- All tax-exempt retirement accounts, including 401(k) and 403(b) plans, as well as defined benefit pension plans

- Any federal benefits that you receive, such as Social Security, Unemployment or Veterans benefits

- Recovery money, such as wrongful death recovery and personal injury recovery and lost earnings payments

- Real property up to $23,675 in value or unused homestead exemption up to $23,675 in equity

All the values listed double if you are married and filing for bankruptcy jointly. So, instead of $1,600 in jewelry, you can keep up to $3,200. That also includes the homestead exemption, so if you’re married the exemption jumps up to $47,350.

Keep in mind that many states allow for higher exemptions. So, depending on where you live sometimes the exemption can go as high as $150,000 for married couples. That means that in many cases, you may be able to save your home from liquidation even though you filed for Chapter 7.

How to rebuild credit after Chapter 7

A Chapter 7 filing creates a negative item in your credit report that remains for 10 years from the date of filing. However, this doesn’t mean that you will have to wait around for a decade before your credit recovers.

In the U.S. credit system, the “weight” of negative items diminishes over time, even though the item remains on your report. So, for instance, a late payment made last month hurts your credit much worse than one made five years ago. This means that the further you get away from final discharge of your bankruptcy, the less it hurts your credit score.

You can basically start taking steps to rebuild your credit starting the day after your final discharge. With your fresh financial start, you also want to include a concerted effort to become creditworthy faster. Here are some tips to help you get started:

- Get a secured credit card or a small personal loan so you can start building a positive payment history.

- Gradually add new accounts, making sure not to take on too much new debt at once; adding debt to quickly is bad for your budget AND credit score.

- Make sure to keep your credit utilization ratio at less than 10%. That means that you only use ten percent or less of your available credit line.

- Once your score starts to improve after about six months, consider other “good” debt, such as an auto loan.

This strategy can pull you out of subprime credit in as little as a year, depending on your history and overall score.

Filing for Chapter 7 again

If you have already filed for Chapter 7 bankruptcy once and then get back into trouble, you can file again. However, while you can file as often as you want, there’s a time window on discharge. Basically, you won’t be eligible for another round of discharge until a certain amount of time has passed.

The clock always runs from the date of your first filing:

- If you filed for Chapter 7 before and want to file for Chapter 7 again, you must wait 8 years

- The window is only 4 years if you filed Chapter 7 before and now want to file Chapter 13

- If your first filing was Chapter 13 and now you want to file for Chapter 7, the gap is 6 years. However, if you paid back all your unsecured debt in-full or paid at least 70 percent, you may be able to file sooner.

Do I need an attorney to file Chapter 7?

By law, you don’t. Just like with Chapter 13 filings, you can file for Chapter 7 “pro se” (Latin for “for oneself”). However, the U.S. courts website actually states, “While individuals can file a bankruptcy case without an attorney or “pro se,” it is extremely difficult to do it successfully.”

So, basically, even the courts say that you’re crazy to do this on your own unless you’re a bankruptcy attorney. And always keep in mind that an attorney may have more success. They’re more experienced at fighting discharge objections. They can also argue the discharge of your student loans and other debts that don’ts easily qualify for discharge.

That’s why it’s always recommended to work with a professional when it comes to bankruptcy.