With age comes wisdom — except about being old, apparently.

A survey from Charles Schwab polled nearly 1,000 people ages 30-79 with an annual income of $35,000 or more. The investment firm probed our beliefs about money and identified several retirement-related myths most of us fall for.

While more than half claimed they were “very or extremely savvy about personal finance,” Schwab makes the case we’re not savvy enough…

Some of these things are up for debate or have important caveats, but most of them are obviously wrong. Let’s go point by point…

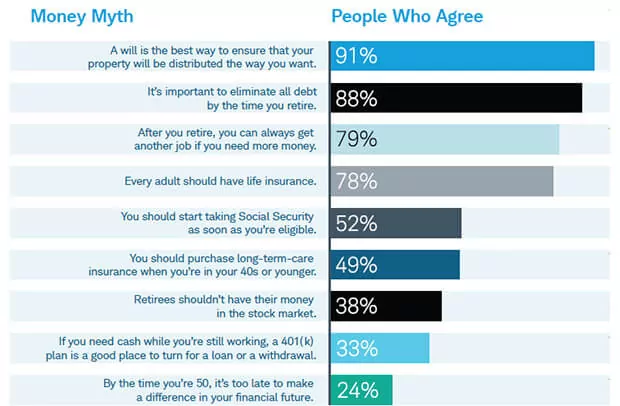

1. “A will is the best way to ensure your property will be distributed the way you want.”

Your will can be overruled.

As The Wall Street Journal explains: If you designate a beneficiary for a 401(k) or bank account, and your will mentions somebody else, the name on the account wins. If you don’t specify a beneficiary, one of two things happens. If it’s a retirement account, the provider has something called a “plan document” that specifies where the money goes. For anything else, your will is usually the official word — if you have one. You should get on that.

2. “It’s important to eliminate all debt by the time you retire.”

This is one of the debatable ones. Not all debt is bad debt…

“If you have a fixed rate mortgage and are receiving a tax break through the mortgage interest deduction, there may be value in continuing to pay the mortgage down on a monthly basis, at least in the near term,” financial services company TIAA-CREF says. More homeowners have mortgages past age 70 than ever before, The New York Times noted last year. What you definitely don’t want is high-interest debt like credit cards.

3. “After you retire, you can always get another job if you need more money.”

It’s getting harder. In the Schwab study, 39 percent plan to work part-time in retirement, but only 4 percent of current retirees actually do. Age discrimination and health issues keep many out work, USA Today says.

4. “Every adult should have life insurance.”

The point of life insurance is to help people after you die. If there’s nobody who needs your help, don’t waste money on life insurance. Here’s what Kiplinger tells single people: “Sad though your death would be, it’s unlikely it would create financial hardship for anyone.” The best candidates for life insurance are parents with minor children and couples with only one income.

5. “You should start taking Social Security as soon as you’re eligible.”

It’s closer to the opposite. You should wait until you need it or age 70, because the amount you receive increases with the delay.

From the Social Security website, which is in slight need of updating…

“The maximum [monthly] benefit depends on the age you retire. For example, if you retire at your full retirement age in 2013, your maximum benefit would be $2,533. But if you retire at age 62 in 2013, your maximum benefit would be $1,923. If you retire at age 70 in 2013, your maximum benefit would be $3,350.”

Do you want up to $23,000 a year, or up to $40,000?

6. “You should purchase long-term care insurance when you’re in your 40s or younger.”

It’s true that the prices are lower when you’re younger, but that doesn’t mean it’s cheaper — you’re just paying for it longer.

But you don’t want to wait too long, either. Says NerdWallet: “The total amount you pay in is lower if you start when you’re 55 than when you’re 70.” The longer you wait, the higher the premiums and the lower the benefits. Your mid-50s are the ideal time to buy, says the American Association for Long-Term Care Insurance.

7. “Retirees shouldn’t have their money in the stock market.”

This is another debatable one, and it all depends on your tolerance for risk. The old rule of thumb is to subtract your age from 100. That’s the percentage of your nest egg you should have in stocks.

By that standard, it wouldn’t be unusual to have a third of your money in stock mutual funds during retirement. But some experts have recently suggested retirees should tread lightly as they enter retirement, and then gradually rev up the risk again. Research shows a portfolio that starts with 30 percent stocks and finishes at 60 percent stocks performs better on average than one that has 60 percent in stocks throughout.

“You want to have the lowest stock allocation when your portfolio is largest, and that’s going to be right before and after retirement,” Wade Pfau, a retirement-income professor at American College, told The Wall Street Journal. “That’s when you’re most vulnerable to losing wealth.”

8. “If you need cash while you’re still working, a 401(k) plan is a good place to turn for a loan or a withdrawal.”

Borrowing $50,000 for five years at a low interest rate sounds great, but it’s generally considered a risky, last-resort idea. If you leave your job, you have to repay the balance within two months or get hit with a big, fat 10 percent tax penalty. Meanwhile, that money isn’t growing for retirement.

9. “By the time you’re 50, it’s too late to make a difference in your financial future.”

Better late than never. Retirement plans are designed to help late savers through what the IRS calls catch-up contributions. If you’re age 50 or older, you can contribute an extra $5,500 per year to a 401(k) and an extra $1,000 per year to an IRA. There’s plenty of advice online for last-minute retirement planners.

Photo: AAG.com.